Calculate ISA Interest Monthly vs Yearly: What Really Makes a Difference?

When you’re tucking money away in a Cash ISA, you’re not just saving—you’re growing. But here’s the thing: how you grow that money can vary a lot depending on whether your interest is calculated monthly or yearly.

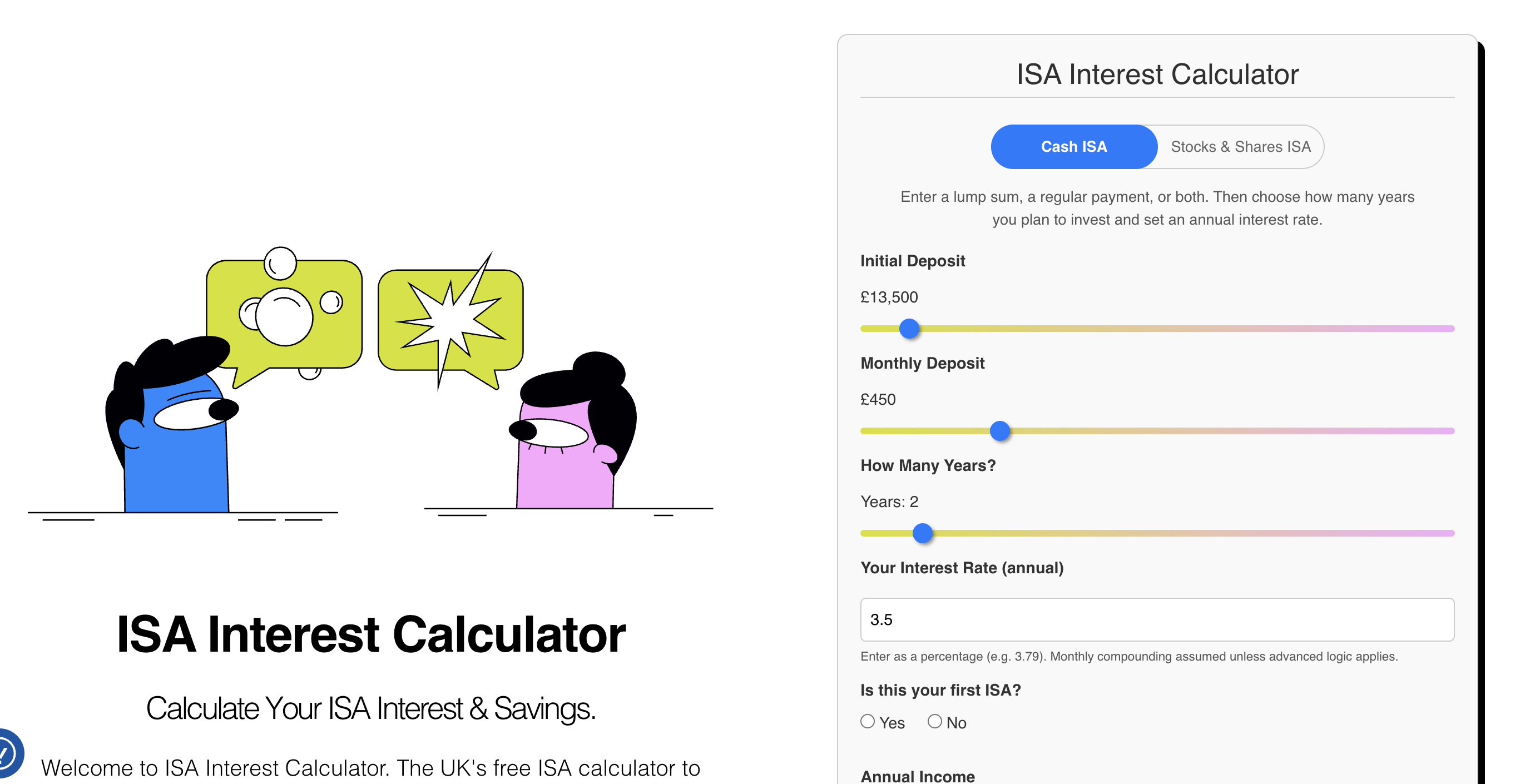

Let’s break it down simply, and I’ll also explain how our ISA Calculator handles this behind the scenes—because yes, we do the maths for you, and yes, we do it monthly. More on that in a sec.

What’s the difference between monthly and yearly interest?

It sounds subtle, but it isn’t. Let’s say you’ve got £10,000 in a Cash ISA at 3.5% interest.

- If the interest is compounded yearly, the bank waits till the end of the year and gives you your 3.5% interest once, all in one go.

- If the interest is compounded monthly, it gets split into 12 smaller bits—around 0.29% per month—but you earn interest on the interest every month.

That monthly compounding? That’s the magic of compound interest working overtime. Because every month your money earns a bit more, and then the next month you earn a bit more on that too. Like a snowball getting bigger as it rolls downhill.

Practical ISA interest example (Barclays & Natwest)

Say you’re considering Barclays, who might offer 3.4% AER on a flexible Cash ISA. That 3.4% is an annual equivalent rate, which usually means the interest is being calculated monthly, but displayed as an annual figure.

Compare that to NatWest, who might advertise a similar rate, but it’s crucial to check whether interest is paid annually or monthly. If it’s paid annually, you’ll miss out on the little monthly boosts that compound over time.

Here’s a real-world example:

- Barclays (monthly compounding): £10,000 at 3.4% monthly compounded over 3 years = £11,062

- NatWest (annual compounding): Same £10,000 at 3.4% yearly compounded = £11,057

It’s not a life-changing difference over three years—but if you’re depositing monthly and doing this over decades? That gap widens.

What does our calculator do?

Good question. Our calculator always compounds monthly, because that’s how most providers calculate it in practice. Plus, if you’re adding regular deposits each month, it makes far more sense.

So when you input your starting amount, your monthly top-ups, and the number of years you’re planning to save, we simulate every single month. Our code breaks time down into 12 parts per year, adds your deposit, applies that month’s slice of the interest rate, and lets the snowball roll.

We even factor in special promo rates, variable rates based on Bank of England predictions, and whether this is your first ISA. But at its core, every calculation we do is based on monthly compounding—because that’s the most realistic way to model real-life ISA growth.

What to do when comparing ISAs

If you’re comparing ISAs, always check how often the interest is applied. Monthly compounding tends to work out better, especially if you’re saving regularly. Banks like Barclays often pay interest monthly, which works in your favour. Some others may only do it yearly.

And remember, our calculator is designed with this in mind. Whether you’re saving £50 or £5,000 a month, we break it all down into monthly chunks so you get a realistic, apples-to-apples picture of your potential returns.

So, play with the sliders, try a few scenarios, and see how much more your money could grow by thinking monthly, not just yearly.

As a UK saver & investor for over 10 years and avid ISA user; James decided to build ISA Interest Calculator to help everyday British savers with calculating potential ISA returns. Having worked for a large FTSE100 company building financial AI tools for over 5 years, he brought his expertise to personal finance and quickly launched several highly-respected and successful finance & investing sites for UK savers and investors.